In January 2023, AbbVie’s most profitable product lost its U.S. patent protection. Humira — at its peak the world’s best-selling drug at $21 billion in annual sales — faced a wave of biosimilar competitors that would cut its U.S. revenue by more than half within two years. Most companies facing that kind of revenue cliff would have slashed headcount. AbbVie mostly didn’t.

Adjusted SG&A held at 20–24% of revenue through the entire transition. The sales reps, medical liaisons, and marketing staff that had built Humira into a franchise stayed largely intact. By 2025, with Skyrizi and Rinvoq combining for nearly $19 billion in revenue, the bet looked right. But whether it constitutes good stewardship or structural inertia depends on how you read the pharmaceutical industry’s incentives.

The Machine Held

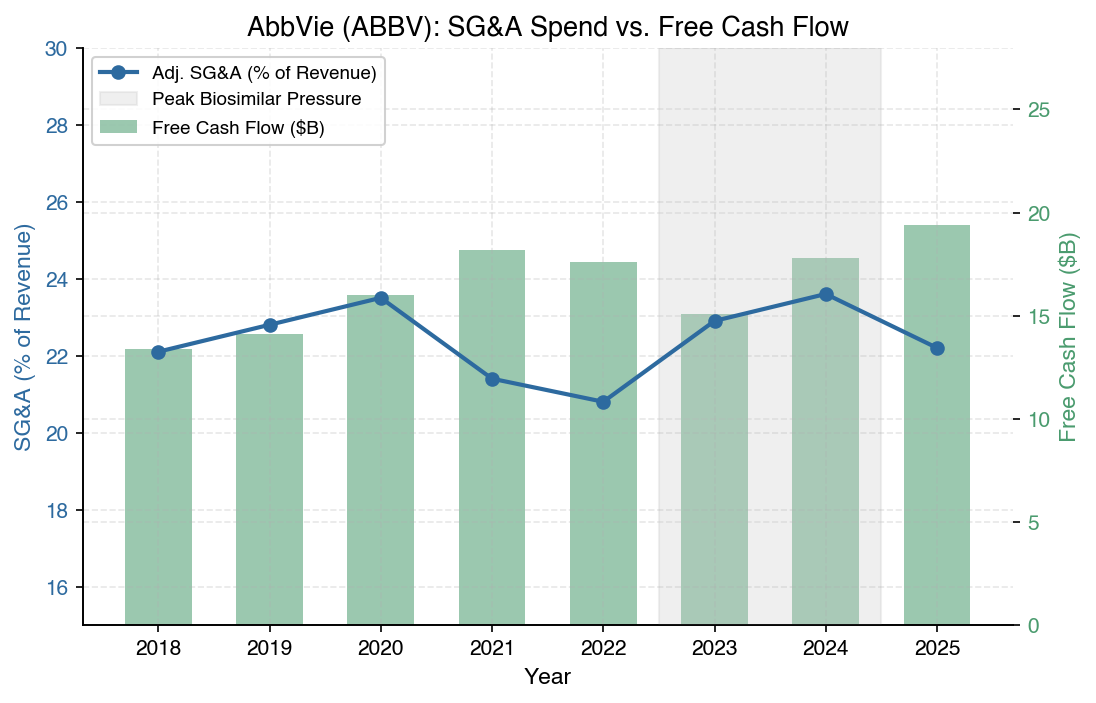

Despite Humira’s collapse — U.S. sales fell roughly 54% year-over-year in 2024 — AbbVie generated $17.8 billion in free cash flow. For every dollar spent on SG&A (approximately $14.2 billion adjusted), it generated $1.25 in free cash flow.

AbbVie’s adjusted SG&A as a percentage of revenue versus free cash flow, 2018–2025. The gray band marks peak biosimilar pressure (2023–2024). Data from AbbVie investor relations and SEC EDGAR.

AbbVie’s adjusted SG&A as a percentage of revenue versus free cash flow, 2018–2025. The gray band marks peak biosimilar pressure (2023–2024). Data from AbbVie investor relations and SEC EDGAR.

By 2025, operating margins had expanded 8.4 percentage points year-over-year — not despite maintaining SG&A, but because the commercial infrastructure was already built. Skyrizi and Rinvoq scaled into a sales force that Humira had funded. The cost was already paid.

Middle of the Pack, by Design

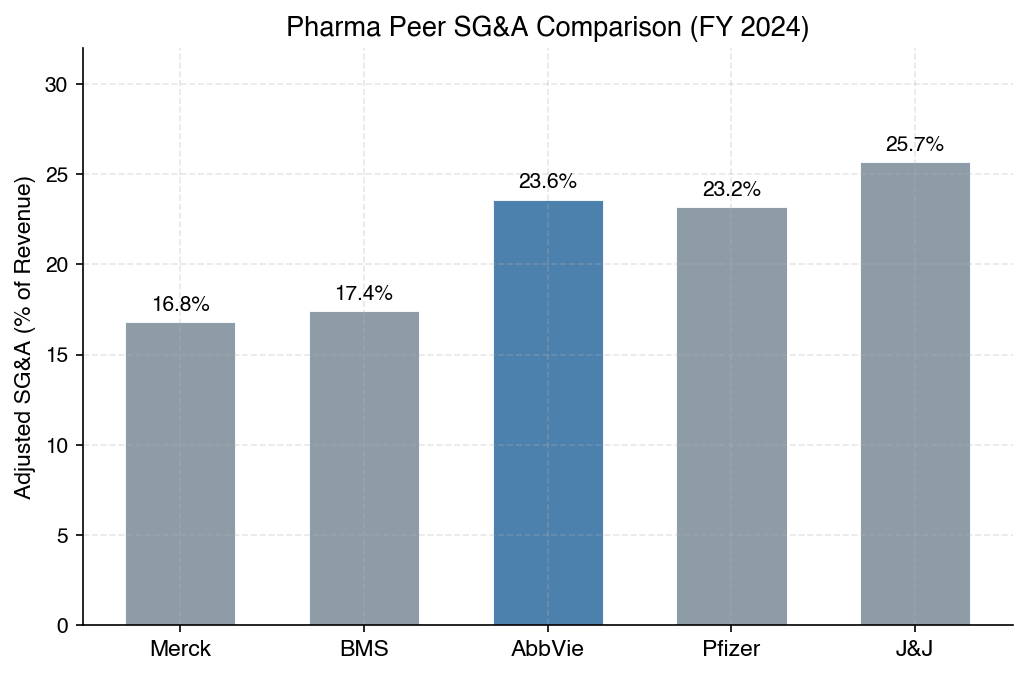

At 23.6% of revenue, AbbVie’s SG&A sits between Merck (16.8%) and Johnson & Johnson (25.7%), roughly in line with Pfizer (23.2%) and above Bristol-Myers Squibb (17.4%).

Adjusted SG&A as a percentage of revenue across major pharmaceutical companies, fiscal year 2024. Sources: company 10-K and earnings releases.

Adjusted SG&A as a percentage of revenue across major pharmaceutical companies, fiscal year 2024. Sources: company 10-K and earnings releases.

The pharmaceutical industry as a whole allocates a significant share of revenue to commercial operations — historically over 40% before recent compression. AbbVie at 22–24% isn’t an outlier. It’s a company operating within the industry’s structural norms. Which raises the harder question.

The Prisoner’s Dilemma

If every major pharma company allocates a quarter of revenue to SG&A, the question isn’t whether AbbVie spends too much. It’s what would happen if the industry spent less.

Specialty drugs like Skyrizi and Rinvoq require high-touch commercial models. Rheumatologists need to be educated on complex immunology data. Medical liaisons answer clinical questions. Patient support programs navigate reimbursement. These are real, specialized jobs — not billboards.

But if all major pharma companies simultaneously cut SG&A by 15%, would Skyrizi’s market share change materially? Would patients receive worse care? Probably not, or not proportionally. Each company is rational to maintain its commercial presence; collectively, the industry sustains an equilibrium that benefits no single company but that no single company can defect from unilaterally. Economists call this a prisoner’s dilemma. In pharma, it takes the form of armies of sales representatives.

What Makes AbbVie Different

AbbVie doesn’t escape this dynamic. The case for the company is narrower: it navigated a rare moment of forced transition without destroying its commercial capacity, and used that continuity to execute one of the largest product portfolio pivots in pharmaceutical history.

AbbVie’s SG&A is also structurally different from what we see in tech. Adobe compressed SG&A from 13.1% to 6.6% of revenue as subscriptions scaled, decoupling revenue from labor cost. AbbVie’s model keeps them coupled. The medical liaison visiting a rheumatologist’s office cannot be replaced by a chatbot. The patient educator walking a newly diagnosed Crohn’s patient through a self-injection protocol is doing work that resists automation. The workers are not being optimized away.

Whether that coupling reflects genuine value or industry-wide inefficiency is the question the data can’t fully answer. What it can show is that AbbVie maintained $17.8 billion in free cash flow through one of the hardest pharmaceutical transitions on record, workforce intact. That’s either exceptional capital stewardship or a well-managed version of a collective action problem.

Probably both.

Data Sources

- Corporate financials: SEC EDGAR — AbbVie Inc. 10-K filings

- Peer comparisons: Company earnings releases and 10-K filings (J&J, Pfizer, Merck, BMS)

- Industry SG&A trends: Statista

- Analysis: Generated by AI (Anthropic Claude), reviewed by Stephen Sciortino