In 2013, Adobe killed its most profitable product. Creative Suite had been a cash machine — customers paid $1,300 up front, and Adobe kept the margins. Replacing it with a $54/month subscription was, by the numbers, an act of self-destruction. For every dollar Adobe spent running the business that year, it kept just 56 cents in profit. The year before, it had kept $1.91.

The bet paid off — spectacularly, and in ways that reveal something important about how subscription economics reshape the calculus of a business. Adobe just posted record Q1 2026 revenue of $6.40B with 12% growth. But the real story isn’t revenue growth. It’s what happened to the ratio of revenue and profits to the cost of running the company.

Three Eras of Adobe’s Business Math

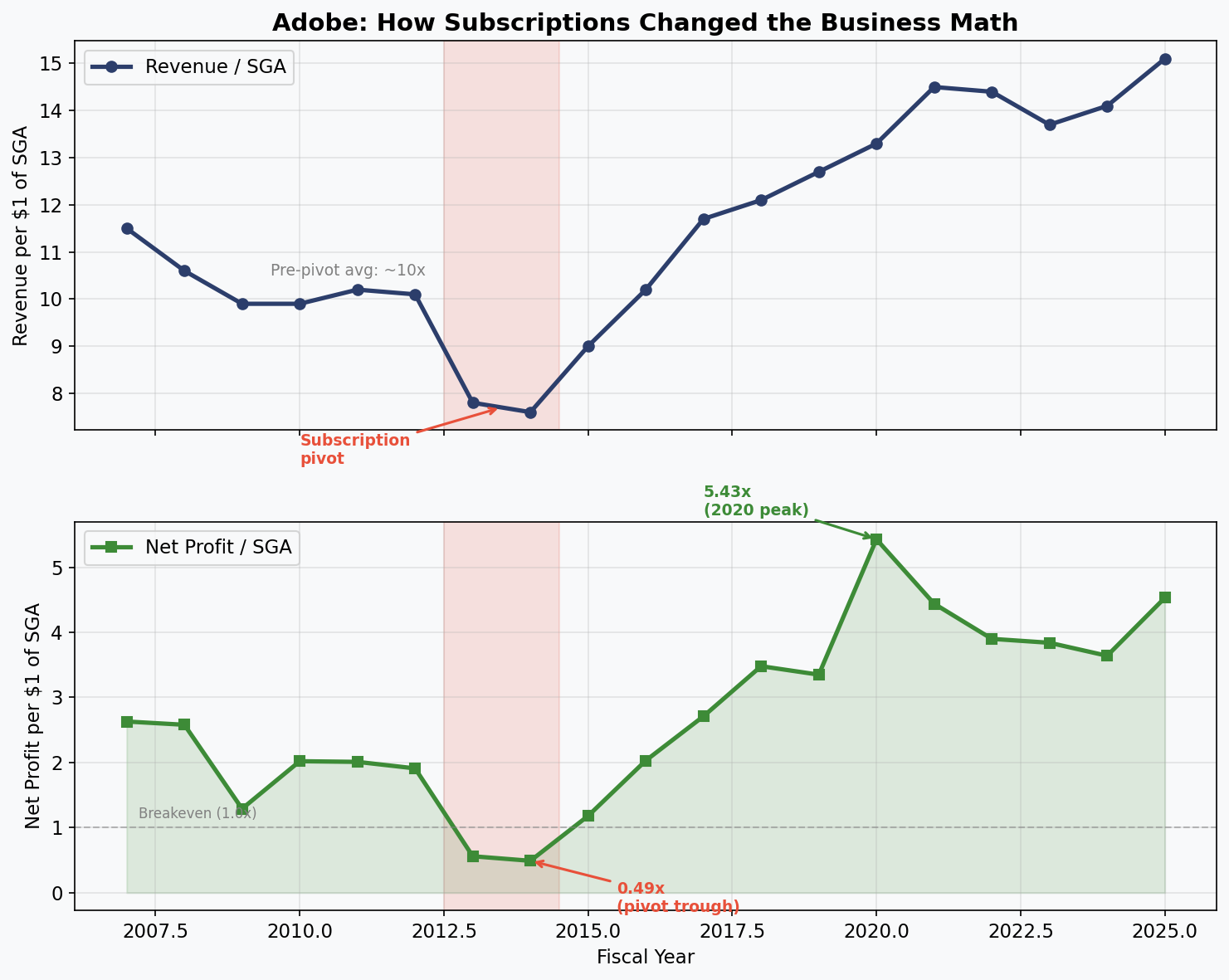

The clearest way to see the subscription model’s impact is through two ratios: revenue per dollar of SGA (selling, general, and administrative expenses — the cost of running the business), and net profit per dollar of SGA.

Top: revenue generated per dollar of SGA. Bottom: net profit per dollar of SGA. The red band marks the subscription pivot (2013-2014). Data from SEC EDGAR XBRL filings.

Top: revenue generated per dollar of SGA. Bottom: net profit per dollar of SGA. The red band marks the subscription pivot (2013-2014). Data from SEC EDGAR XBRL filings.

Pre-pivot (2007-2012): Adobe generated roughly $10 in revenue for every $1 of SGA, and about $2 in profit. Stable, predictable, unremarkable. The perpetual license model had a ceiling — growth required selling more boxes to new customers, and each sale needed proportional sales and marketing effort.

The pivot trough (2013-2014): Both ratios cratered. Revenue per SGA dollar dropped to 7.6x as subscription revenue trickled in while SGA costs spiked to support the transition. Profit per SGA dollar hit 0.49x — Adobe was spending more than twice on overhead what it was keeping in profit. This is the moment most companies would have reversed course.

Post-pivot (2015-2025): The subscription flywheel kicked in. Revenue per SGA dollar climbed steadily past the old ceiling to 15.1x in 2025 — 50% higher than anything Adobe achieved selling boxed software. Profit per SGA dollar surged to 4.53x, more than double the pre-pivot average and nine times the trough.

Why Subscriptions Change the Math

The mechanism is straightforward but its scale is striking. Under the perpetual model, SGA costs scaled roughly in proportion to revenue — selling more copies required more salespeople, more marketing, more support. The subscription model broke that relationship.

Once a customer is on Creative Cloud, renewal is automatic. There’s no re-selling cost. The marketing spend that acquired a customer in year one generates revenue in years two, three, and beyond with minimal incremental SGA. Adobe’s SGA as a percentage of revenue compressed from 13.1% at the pivot to 6.6% in 2025 (per SEC EDGAR filings) — not because Adobe spent less in absolute dollars (SGA tripled from $540M to $1.57B), but because revenue grew six times faster.

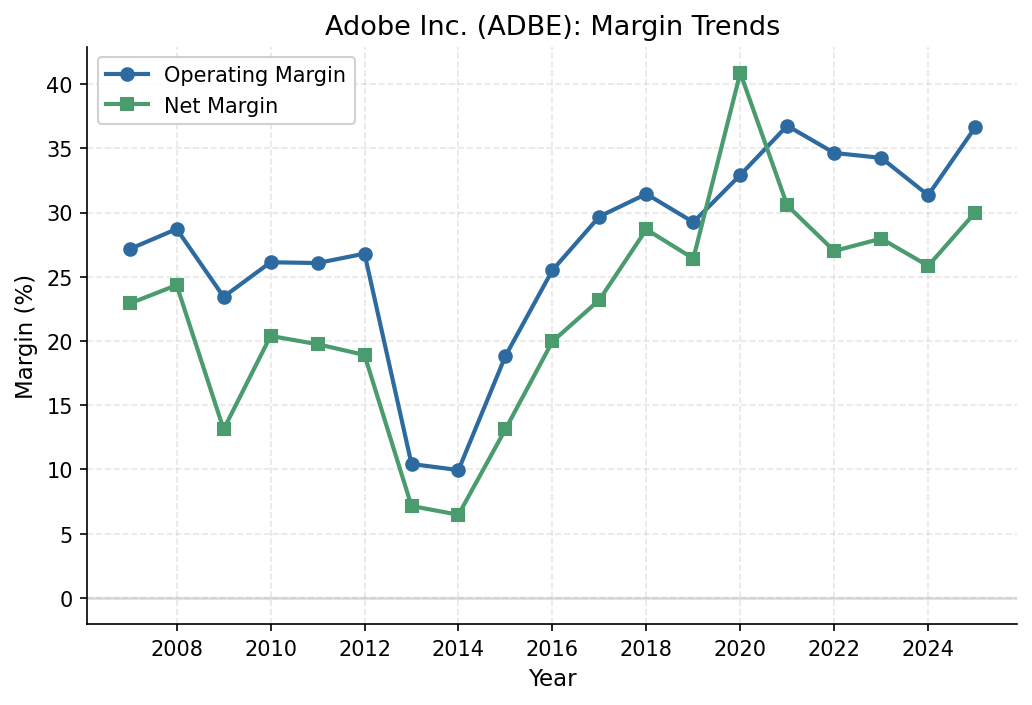

Operating and net margins from 2007-2025. The subscription pivot created a permanent step-change in profitability.

Operating and net margins from 2007-2025. The subscription pivot created a permanent step-change in profitability.

Operating margins tell the same story from a different angle. Pre-pivot margins hovered around 26-28%. Post-pivot, they’ve settled in the 31-37% range — a structural improvement that shows no signs of reverting.

The Labor Implications

This is where the business math becomes a labor story. Adobe’s 30,600 employees each generate $703,000 in revenue and $182,000 in profit. Those are impressive numbers, but the trend matters more than the snapshot.

When profit per dollar of SGA goes from 2x to 4.5x, the excess value has to go somewhere. It’s not going to SGA (which includes employee compensation) — that ratio is compressing. It’s going to shareholders via margins and buybacks. National average hourly earnings grew 3.8% year-over-year per BLS data, and real wages grew just 1.2% after inflation per FRED. Adobe’s profits grew 10x over the same period.

The subscription model didn’t just change Adobe’s revenue. It changed the leverage between capital and labor. Every dollar of worker effort now generates more revenue that the company keeps more of. The workers are more productive, but the gains accrue disproportionately to the business.

A Story That Already Came True

This isn’t a warning about what might happen — it already has. Adobe was early, but the rest of the industry followed. Microsoft moved Office to 365. Autodesk converted AutoCAD. Salesforce was subscription-native from day one. Today, virtually every major software company runs on recurring revenue. Each conversion followed the same pattern Adobe pioneered: short-term pain, then permanently higher ratios of revenue and profit to overhead.

The result is an entire industry that has structurally decoupled revenue growth from workforce growth. Adobe’s 30,600 employees serve hundreds of millions of users. The information/technology sector shed 5.8% of its workforce last year per BLS even as companies like Adobe posted record revenue.

Adobe democratized creative tools — that’s real value. But the subscription math shows that the model’s greatest efficiency isn’t serving customers better. It’s decoupling revenue growth from the people who make it possible.

Data Sources

- Corporate financials: SEC EDGAR — Adobe Inc. 10-K filings (2007-2025)

- Sector employment: Bureau of Labor Statistics — Current Employment Statistics

- Wage data: FRED — CPI-adjusted hourly earnings

- Analysis: Generated by AI (Anthropic Claude), reviewed by Stephen Sciortino